Key Takeaways

- Harassment is never acceptable, even if a borrower has fallen behind on repayments. A licensed moneylender and anyone acting on its behalf must still recover debts lawfully.

- Borrowers are protected by the law. You are entitled to clear loan documents, statements of account, and safeguards on interest, late interest, fees, and total applicable charges.

- Keep records diligently. Save messages, call logs, screenshots, and details of any visits—they are crucial if you need to prove misconduct.

- Know where to get help. You can lodge a complaint with the Registry of Moneylenders and the police if there are threats, intimidation, or violence involved.

Picture this: You forgot to make a repayment to your licensed moneylender this month, and the next thing you know, you’re on the receiving end of repeated calls and threatening messages. This is a classic example of licensed moneylender harassment. While uncommon, licensed moneylender harassment can still happen and take a serious emotional toll on the borrower.

No matter the situation, remember this: harassment is never acceptable. Falling behind on your loan repayments does not give any lender or debt collector the right to threaten, shame, or intimidate you.

So, how do you know if you’re a victim of licensed moneylender harassment, and how can you file a complaint against a licensed moneylender? Read on to find out.

What Counts as Licensed Moneylender Harassment?

Contrary to popular belief, licensed moneylender harassment isn’t just about threats; it includes any debt recovery method that intimidates, humiliates, or intrudes unnecessarily into your life. Licensed lenders are responsible for the conduct of the debt collectors they engage—whether in-house or external—and for ensuring that debt recovery is conducted professionally at all times.

Examples of licensed moneylender harassment include:

- Persistent or excessive contact: Unreasonable repeated calls or messages or contact outside restricted hours—generally 8 am to 10 pm on weekdays and 9 am to 9 pm on weekends/public holidays, unless you’ve given written consent.

- Threatening or abusive behaviour: Using language or actions intended to scare, shame, or pressure the borrower.

- Public humiliation: Exposing details of your debt to your family, neighbours, coworkers, or on social media.

- Intrusive visits: Turning up at your home or workplace unnecessarily without first using less intrusive methods.

Your Rights as a Borrower in Singapore

Falling behind on repayments does not mean you lose your rights as a borrower. Even if your loan is overdue, a licensed moneylender must still follow the law, stick to the agreed terms, and treat you fairly and professionally at all times.

First and foremost, you are entitled to clear documentation, including a written loan contract and up-to-date statements of account, so you have full visibility of what has been borrowed and repaid.

This protection also extends to the cost of borrowing. For personal loans, the interest rate is capped at 4% per month; the late interest rate is capped at 4% per month on overdue amounts only; late fees cannot exceed S$60 per month, regardless of your loan size; and administrative fees cannot exceed 10% of the principal. In addition, the total recoverable amount (interest + late interest + all applicable fees) must not exceed 100% of the original principal.

If a lender breaches these rules or harasses you, you have grounds to lodge a complaint against a licensed moneylender.

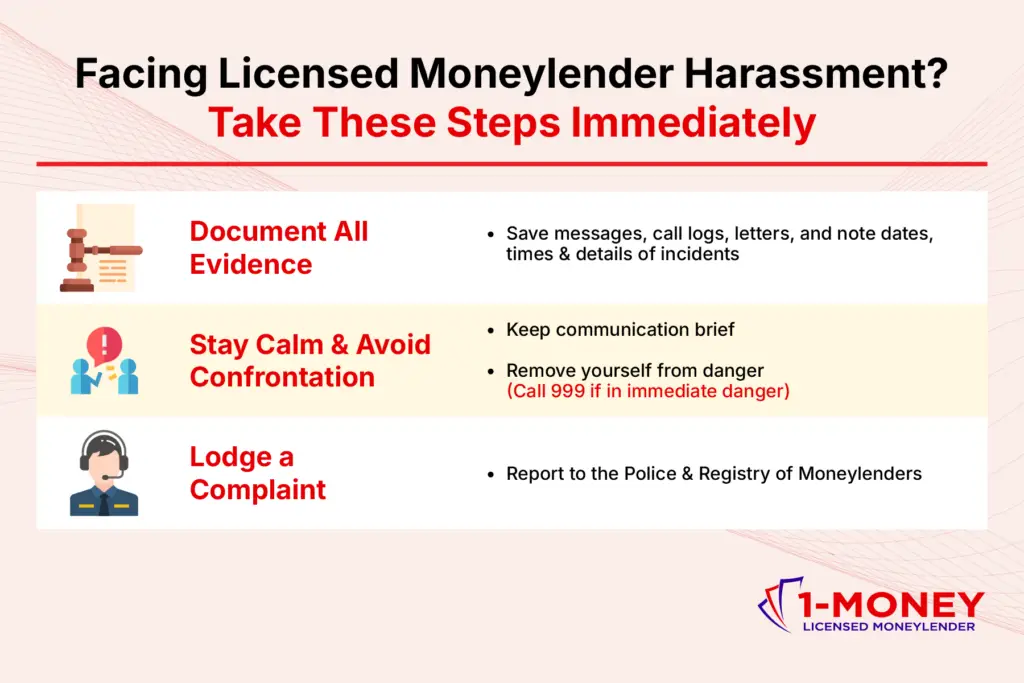

Facing Licensed Moneylender Harassment? Take These Steps Immediately

#1 Document All Evidence

Start by keeping a detailed record of all interactions. Save WhatsApp/text messages, call logs, voicemails, and photos of any letters or notices. Also note the dates, time, location, and names of the people involved in the incident(s) you wish to report. It’ll be helpful to write down the details of what happened as soon as you can, while your memory is still fresh. This will make it easier to show a pattern of harassment, which is essential for filing a complaint against a moneylender.

#2 Stay Calm and Avoid Confrontation

Try to avoid getting into an argument with your licensed lender, even if it’s difficult to keep your cool in the heat of the moment. Keep communication brief and factual, and focus on preserving evidence. Always prioritise your safety: do not feel pressured to respond immediately or continue the interaction longer than necessary, and remove yourself from situations where you feel threatened. Call 999 if you are in immediate danger.

#3 Lodge a Complaint Against a Licensed Moneylender

If your licensed lender crosses the line, report it. For cases involving licensed moneylender harassment resulting in threats to your safety, please lodge a police report on top of reporting the matter to the Registry of Moneylenders. Having all of the relevant evidence on hand could potentially speed up investigations.

Note that the Registry of Moneylenders only handles complaints related to licensed moneylenders; if you find yourself in trouble with unlicensed moneylenders, report the matter to the police immediately.

What Happens After You Lodge A Complaint Against A Licensed Moneylender

Once a complaint against a licensed moneylender is filed, the Registry of Moneylenders will commence investigations and may contact you for further clarification or documentation. Rest assured that all complaints are taken seriously and will be thoroughly investigated; any moneylender found to have violated regulations under the Moneylenders Act will face legal consequences, including licence suspension or revocation, fines, and even imprisonment.

Should You Continue Repayment During a Dispute?

Yes—even if you’ve filed a complaint against a moneylender, your rightful loan repayment obligation—in accordance with your loan contract—remains in effect until a formal decision is reached by the Registry of Moneylenders or the courts. A complaint against a licensed moneylender does not automatically cancel the loan or pause your repayment schedule.

Similarly, if a lender’s licence is suspended or revoked, loans signed before that decision remain valid and enforceable under the Moneylenders Act.

If making full repayment is difficult, do not simply stop paying without any communication. Instead, write to the lender formally by email or letter, explain your circumstances honestly, and keep copies of all correspondence. Licensed lenders are generally open to making alternative repayment arrangements if a borrower is facing genuine financial hardship; just remember to request a written record if a new repayment agreement is reached.

Conclusion

The bottom line is this: you don’t have to tolerate licensed moneylender harassment; missed repayments do not give lenders the right to do whatever they wish. If you ever experience improper conduct, do not hesitate to report it to the authorities.

For a safe and transparent borrowing experience, consider 1-Money, a trusted licensed moneylender in Singapore. Ready to take the next step? Reach out to us for an obligation-free chat about your options or send in an online application. You can also check out reviews by our customers for added reassurance.